Free Sample Academic Papers

Project Evaluation

- AWB ADMIN

- Samples

- Hits: 1064

Introduction

A project refers to a set of activities, which are limited in scope, space and time to achieve specific objectives. Since these resources are always limited, a detailed evaluation should be carried out before settling on one project as the most optimal options. It is important to carryout evaluation before actual execution of the project to avoid foreseeable mistakes as well as allow maximization of resources. Project evaluation and selection is an important phase of project cycle, which is motivated by the desire to establish chances of success for a proposed project. It is also important to evaluate projects to enable informed decision making when choosing from various alternative options (Bruce, 2003).

In general, Project Evaluation involves the control of planning and implementation of activities of a project in relation to the desired objectives. It assesses major consequences of a proposed project and gives quantitative information to guide policy decision makers. Thus, project evaluation is generally the basis of large decision-making processes. The project parties often make decisions to conduct project evaluations by signing the project document. In most cases, the desirable goals of an organization may be achieved through various projects. Once the objective or an organization has been established, the executives invite various options either from in-house engineers or outside contractors. The received alternatives of achieving organizational goals carry varying constraints and resource requirements. This situation makes it necessary to carry out an evaluation on the projects to establish the option, which will ensure realization of organizational goals in the cheapest means possible (Rogers, 2001). This paper explains what it entails to carry out a project evaluation before settling on the most appropriate option.

Types of Project Evaluation

The process of project evaluation is considerably tedious because it involves a myriad of constraints. Project constraints, which are useful in the evaluation process, may be measurable or not. As a result, the process entails a threefold analysis encompassing quantitative, qualitative as well as integrated techniques. The following sections examine these three approaches applied in evaluating a project. The uniqueness of organizational project evaluation techniques does not make these methods meaningless. Instead, all the procedures employed by organization in project evaluation process fall in any of the three categories.

Looking for Project Evaluation Assignment Writing Assistance? ORDER HERE

Quantitative Approaches

Quantitative approach is commonly used in most organizations because of its ease in comparison. The approach applies quantifiable decision-making parameters like cash flows, rate of employment, profit margins and sales revenues among others. This approach is usually the most reliable since if the anticipated expenditure and revenue are correct. The estimates are converted in to net present values, which make it easy to do comparison between various project alternatives (Hans, 2005).

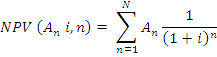

NPV Comparison

The Net Present Value evaluates the present value of a business if it is execute to the end. It establishes the foreseeable cash flows both outwards and inwards prior to the execution. The assumption of this method is that all the cash outflows and inflows are known with certainty. It also incorporate aspect of time value of money, which postulates that money, is of a higher value if held currently than in a future (Babcock & Morse, 2001). Therefore, this method uses discounted values of projected revenue and investments costs in calculation of the present worth of a business. The discounting factor is the obtained from the effective interest rate. The equation below shows how net future cash flows are discounted to show their present values (Hans, 2005).

An is the net cash flow of an nth period and i is the interest rate. The selection criterion of an acceptable project depends on the value of NPV obtained from the computation. The project alternative with the highest value of NPV is desirable. Using this method implies that non-measurable decision parameters are not important or impossible to incorporate in the decision process. An outstanding weakness of this evaluation technique is its inability to measure projects with various scopes. Taking the overall net present value alone as a measure of performance is not sufficient to show efficiency.

Return on Investment

Every business venture is aimed at making profits. For every investment commitment, investors are motivated by the possible returns from their projects. During the evaluation process, it is important to incorporate this measure of performance by establishing the potential return on investment. It is the ratio of net cash inflows to the outlaid amount. The net cash inflow is the annual revenue less associated operational cost.

The project with the highest value of ROI is desirable because it shows the potential of maximizing investors’ resources (DeFusco, McLeavey, Pinto, & Runkle, 2011).

Payback Period Comparison

Payback period is another method of comparing project options. The method measures the length of time required to realize invested capital from net revenues. It is a simple and quick measure of project’s viability. Among the many project accepted as options, the one with the shortest payback period is desirable. This is in line with most investor’s psychology of anticipating returns in the shortest time possible. In other words, it is the breakeven point where cumulative net present values of sequential years just meet the initial outlay (Hans, 2005). It is given by:

The conspicuous limitation of this method is in its failure to consider time value of money and projects performance after breakeven point. Paying attention to payback period exclusively may not be the best method because there are other aspects of project measured up on completion only.

Pacifico and Sobelman Project ratings

This method seeks to establish the most reliable quantitative method of project evaluation by sealing the gaps left by the aforementioned methods. It seeks to solve the assumption that the values of decision-making parameters are known with certainty. Carl Pacifico developed a project-rating factor to assist in evaluating project performance by incorporating the probabilities of both technical and commercial successes.

Project rating factor is given by:

Where pT and pC are the probabilities of technical and commercial successes respectively. R is the total revenue possible throughout project life cycle while TC is the total investment.

Conversely, project value factor is computed as:

Where P is the profit per year, TLC is the estimated product life cycle, C is the mean annual development cost and TD is years of development.

Using these factors, organizations evaluate the possible alternatives with a bid of selecting an option with the highest factor.

Qualitative Approaches

Despite being famous among project managers, qualitative approaches of project evaluation are not always the ideal means of making the most optimal decision. This is occasioned by the fact that some decision-making parameters are not sufficiently quantifiable. In such cases, it becomes prudent to do a qualitative analysis. Qualitative techniques like decision trees, focus groups, benchmarking, and nominal group technology. These techniques are collectively used through collective multifunctional evaluations.

Collective Multifunctional Evaluation

In collective multifunctional evaluation experts seek establish acceptance criteria by merging both quantitative and qualitative methods. Once all the factors considered as important in determining projects’ successes, these experts weigh them in order of importance or range of impact. Out of these results, a project with the highest score of acceptability is selected.

Conclusion

The objective of evaluation is to establish the merit or worth of products, projects, procedures and processes. Well-planned evaluations provide information that aid in explanation of outcomes. Project managers frequently face the challenges of evaluating innovations and finding out progresses or goals achievements. While carrying out a project evaluation, it is important to underscore that fact that business environment is highly dynamic. The use of traditional quantitative methods is not enough to inform a decision of selection a project. Conversely, the use of quantitative methods alone is not sufficient too in the decision making process. Consequently, seeking a means that incorporates the two frontiers will ensure that a suitably informed selection is done by decision-making organ in an organization. It is also important for evaluators to ensure that they capture all the information that matter prior to making conclusions.

References

Babcock, D. L. & Morse, L. C. (2001). Managing Engineering and Technology. Sydney:

Prentice-Hall, Sydney.

Bruce, J. F. (2003). Investment Performance Measurement. New Jersey: John Wiley & Sons.

DeFusco, R. A., McLeavey, D. W., Pinto, J. E., & Runkle, D. E. (2011). Quantitative Investment

Analysis. New Jersey: John Wiley and Sons.

Hans J. T. (2005). Management of Technology. New Jersey: John Wiley & Sons

Rogers, M. G. (2001). Engineering Project Appraisal: The Evaluation of Alternative

Development Schemes. New York: Wiley-Blackwell.